Finance Buyer to Cash Seller Property Transfer in Dubai

- CLC Conveyancing

- Apr 15

- 2 min read

Buying a property in Dubai with finance from a cash seller is one of the more straightforward financed transactions, but it still requires careful coordination.

At CLC Conveyancing, we manage this process from contract through to transfer, ensuring each stage is aligned between the buyer, seller, and bank.

How This Transaction Works

In this structure:

The buyer is purchasing with a mortgage

The seller owns the property outright (no mortgage to settle)

Funds flow directly from the buyer’s bank to the seller at transfer

This removes the complexity of settling existing finance, but introduces bank timelines and approvals.

Step-by-Step Process

Step 1. Offer Agreed & Memorandum of Understanding (Form F)

Once terms are agreed:

Form F is drafted and signed

Deposit is placed (usually 10%)

Mortgage process begins formally

Tip: Ensure the contract includes clear wording around mortgage approval to protect the deposit.

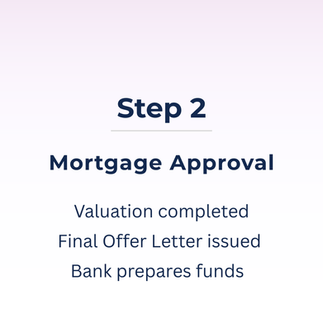

Step 2. Mortgage Process (Buyer Side)

The buyer’s bank will:

Conduct property valuation

Issue the Final Offer Letter (FOL)

Prepare for fund release

This is often the stage that defines the timeline.

Step 3. NOC Application (Developer Approval)

Once the FOL is issued:

NOC is requested from the developer

Seller clears any outstanding service charges

Developer confirms no objections to transfer

Step 4. Pre-Transfer Coordination

At this stage:

Trustee office appointment is scheduled

Manager’s cheques are prepared

Final documents are aligned between all parties

Step 5. Transfer Day

At the trustee office:

Buyer’s bank releases funds

Seller receives payment via manager’s cheque

Title deed is transferred to buyer

Typical Timeline

Mortgage approval & valuation: 2–4 weeks

NOC process: Depends on the developer

Transfer scheduling: within 3-5 days after NOC

Overall: 4–6 weeks

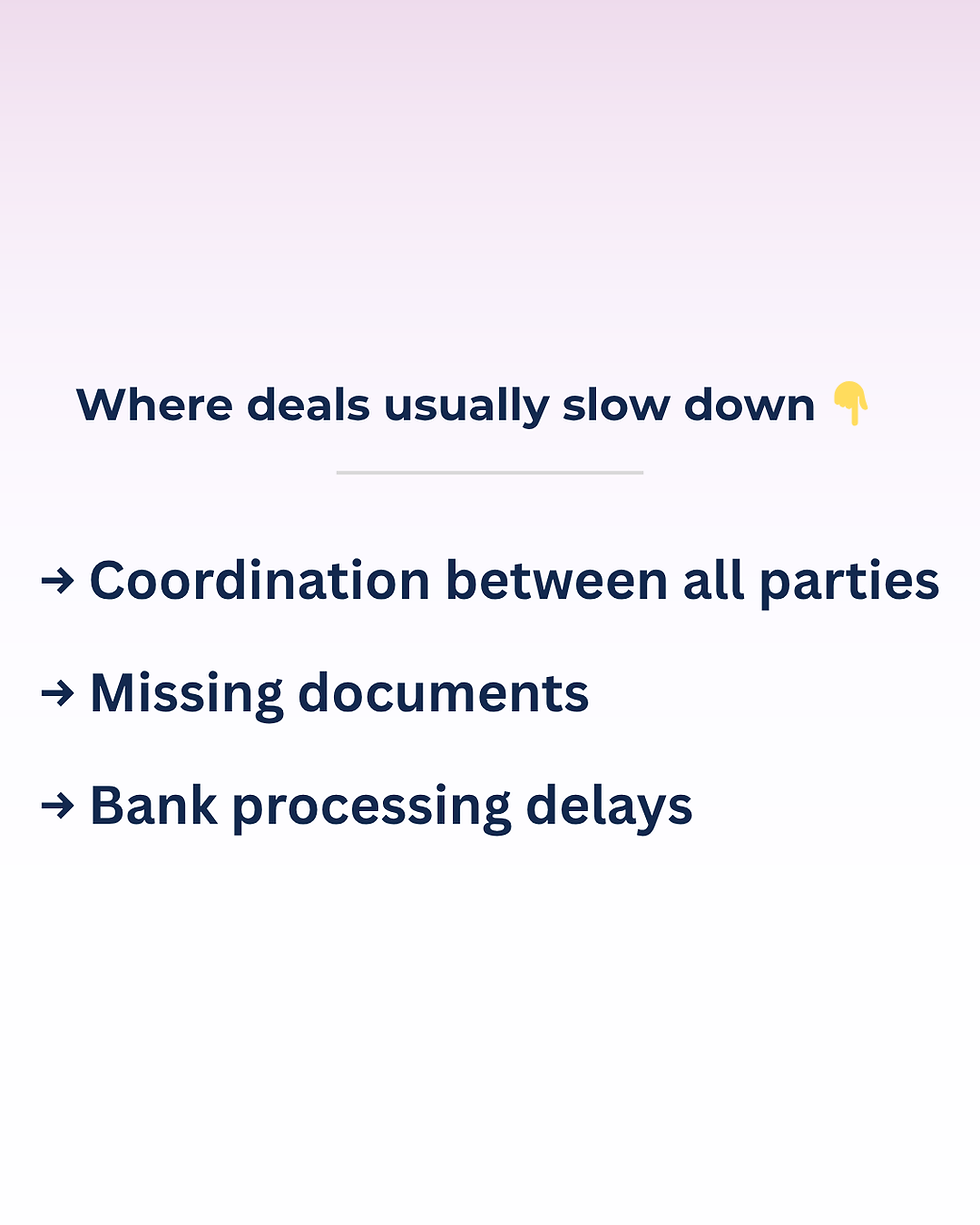

Where Delays Can Happen

Mortgage approval taking longer than expected

Valuation coming in below purchase price

Missing documents or slow coordination

Developer NOC processing times

How CLC Supports This Process

We coordinate:

Communication between buyer, seller, and bank

NOC application and developer requirements

Transfer preparation and appointment booking

Final document and payment alignment

Our role is to keep the transaction structured, clear, and moving forward.

Frequently Asked Questions

Q: Is this simpler than a finance-to-finance transaction?

A: Yes — as there is no seller mortgage to settle, the process is more straightforward.

Q: When does the seller receive funds?

A: On transfer day, once the bank releases the mortgage funds.

Q: Can delays still happen?

A: Yes — mainly on the buyer’s mortgage side or valuation stage.

Q: Do I need a conveyancer for this type of transaction?

A: While not mandatory, coordination across bank, developer, and trustee office is key to keeping timelines on track.

If you’re buying with a mortgage or supporting a client through this process, we can guide you through each stage.

Start your transaction here: https://www.clcconvey.com/start-your-property-transfer